Broker Collusion Costs Traders $1M+/Year. Here's How.

Key Takeaways

- Annual freight spend: $6 million

- Rate premium from collusion: $900,000 to $1.5 million

- Over five years: $4.5 million to $7.5 million

Commodity traders spend months negotiating purchase and sale agreements, managing price risk, and optimizing trading strategies. Then they lose hundreds of thousands of dollars in freight procurement — not because of market conditions, but because of how they run their tenders.

The mechanism is broker collusion. It's widespread, rarely discussed openly, and almost entirely preventable.

How broker collusion works in freight tendering

Freight brokerage is a small, interconnected market. The same 15–30 brokers handle most commodity freight in any given hub — Dubai, Geneva, Singapore, Rotterdam. They know each other. They work together on other deals. They share market intelligence as a matter of course.

When a commodity trader sends a freight tender to five brokers via email, those brokers immediately begin gathering intelligence. Who else received the tender? What's the cargo? What's the trader's urgency level? What are current market rates?

This intelligence gathering happens through informal channels — phone calls, messaging apps, shared contacts. By the time offers come back, brokers have a reasonable picture of what others are bidding. The result is not competitive pricing. It's a coordinated rate floor.

The financial cost

The rate premium from broker collusion in email tendering is typically 15–25% above what a genuinely competitive process would produce.

For a commodity trading desk running 120 tenders per year at an average freight cost of $50,000:

- Annual freight spend: $6 million

- Rate premium from collusion: $900,000 to $1.5 million

- Over five years: $4.5 million to $7.5 million

This is not a theoretical cost. It's a direct transfer of trading margin to brokers — enabled entirely by the email tendering process.

Why email tendering enables collusion

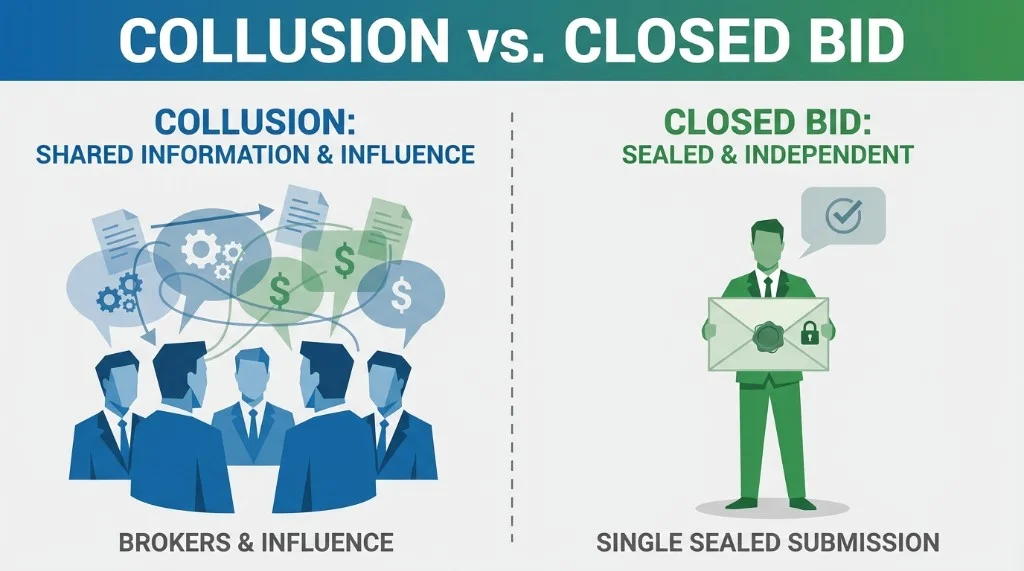

Email tendering has no mechanism for broker isolation. When a tender is sent to multiple brokers simultaneously, there is no control over what information brokers share with each other.

Even without explicit communication between brokers, email tendering enables collusion through:

- Forwarded emails revealing other recipients

- Market signal reading from tender timing and cargo specifications

- Informal market intelligence networks

- Sequential offer revision after learning competitor rates

The closed-bid solution

Closed-bid tendering applies a simple principle borrowed from sealed-bid procurement in other industries: each broker submits their offer without visibility into what others are bidding.

In practice, this means:

- Brokers are invited individually through a controlled platform

- Each broker sees only their own invitation and their own submitted offer

- Offers are submitted simultaneously in standardized format

- Once submitted, offers are immutable — no retroactive revision

- The trader sees all offers in a single comparison table

When brokers cannot see each other's bids, genuine competition is restored. The rate premium from collusion disappears. Across Bench Energy's client base managing $1.2B+ in freight, this has delivered an average 18% rate reduction compared to email tendering.

The compliance dimension

Broker collusion in freight tendering is not just a financial problem. It's a compliance problem.

Regulatory environments for commodity trading are tightening globally — DMCC in Dubai, FINMA in Switzerland, MAS in Singapore. Regulators increasingly expect trading companies to demonstrate that procurement decisions were made through genuine competitive processes.

An email tender with no audit trail and no mechanism for broker isolation is difficult to defend under regulatory scrutiny.

Closed-bid tendering provides an immutable audit log: every invitation, every submission, every award decision — timestamped, logged, and auditable.

What to do now

If your trading desk is still running freight procurement through email, the first step is quantifying the cost.

Multiply your annual freight spend by 15%. That's the conservative estimate of what broker collusion is costing you annually.

Then ask: is the operational convenience of email tendering worth that cost?

How to detect broker collusion

Broker collusion is rarely overt. It operates through informal channels and subtle market signals. But it leaves identifiable patterns that commodity traders can learn to recognise.

The most reliable red flags:

- Rate clustering within 2–3%. When five brokers independently assess a freight route, genuine competition produces a spread of 8–15%. If offers consistently cluster within 2–3% of each other, brokers are likely calibrating against shared intelligence rather than competing independently.

- Consistent winner rotation. In a genuinely competitive market, the lowest-cost broker varies based on vessel availability, positioning, and market conditions. If the same three brokers rotate winning bids in a predictable pattern, it suggests an implicit allocation arrangement.

- Rates consistently above market indices. Compare your awarded rates against the Baltic Dry Index (BDI), Baltic Capesize Index (BCI), and route-specific benchmarks. A persistent premium of 10% or more above index rates — after adjusting for vessel specifications and cargo requirements — indicates non-competitive pricing.

- Suspiciously synchronised submission times. Genuine offers arrive at different times, reflecting different internal processes. If multiple offers arrive within minutes of each other, brokers may be coordinating submission timing to signal their bids.

- Identical terms beyond rate. When multiple brokers submit the same laycan terms, the same vessel class preferences, or identical demurrage clauses, it suggests a shared information source rather than independent analysis.

Track these indicators over 20–30 tenders. Patterns that appear once are noise. Patterns that repeat across a quarter are systemic.

Prevention beyond technology

Closed-bid tendering eliminates the mechanism for collusion. But a robust anti-collusion strategy extends beyond the tendering platform itself.

Broker network diversity. A panel of five brokers is easy to coordinate. A panel of 15–20 brokers is not. Expand your broker network deliberately — include regional specialists, niche operators, and new market entrants alongside established names. The larger and more diverse the panel, the harder it is for brokers to form effective coordination networks.

Rotation and randomisation policies. Never invite the same subset of brokers to every tender. Randomise invitations from your broader panel. This prevents brokers from predicting who they are competing against, which is the foundation of effective collusion.

Blind benchmarking against market indices. After every tender, compare the awarded rate against the relevant Baltic Exchange index, Platts freight assessments, and Clarksons fixtures data. Maintain a rolling benchmark that tracks your rate premium or discount to market. Any sustained premium above 5% warrants investigation.

Automated benchmarking in FreightTender. Instead of commissioning separate consultant audits, the FreightTender dashboard surfaces each award against the Baltic / Platts route curve you choose — blind benchmarking on every fixture, with a full audit trail. You see whether you paid above or below the market strip without an extra project or retainer.

Internal separation of duties. The person who selects which brokers to invite should not be the same person who evaluates offers. This internal control prevents any single individual from steering tenders towards preferred brokers.

Case example: rate impact of switching to closed-bid

Consider a mid-market thermal coal desk based in Dubai / Singapore, running 120 freight tenders per year on routes such as Richards Bay FOB → ARA and India, with an average fixture cost of $50,000 — a total annual freight spend of $6 million (same scale as the worked example earlier in this article). Programme period: Q3 2024–Q1 2026.

Under email tendering, this desk was paying an estimated 15–25% collusion premium. Their internal benchmarking showed awarded rates consistently 18% above Baltic Exchange route equivalents, even after adjusting for vessel specifications and cargo complexity.

After switching to closed-bid tendering through Bench Energy's FreightTender platform:

- Average rate reduction: 18%. Across 120 tenders, this translated to $1.08 million in annual freight savings.

- Procurement cycle: reduced from 4 days to 14 hours. The desk recovered approximately 500 hours of annual admin time.

- Demurrage incidents: reduced by 35%. Faster procurement improved cargo window alignment, saving an additional $168,000 annually.

- Total annual savings: $1.25 million. Against a platform cost that was recovered within the first two months of operation.

The rate improvement was not gradual. It appeared immediately on the first closed-bid tender — because the mechanism driving inflated rates (broker information sharing) was eliminated on day one.

This pattern is consistent across Bench Energy's client base. Desks with higher freight spend see proportionally larger savings, but even smaller desks running 50–60 tenders per year typically recover $400,000–$600,000 annually.

Frequently asked questions

How do freight brokers collude on rates?

Freight brokers collude through informal intelligence networks — phone calls, messaging apps, and shared contacts within the small community of commodity freight brokers. When multiple brokers receive the same email tender, they gather information about competing bids, cargo urgency, and prevailing market conditions. This allows them to coordinate a rate floor rather than compete genuinely. The result is rates 15–25% above what a sealed, competitive process would produce. Collusion is rarely explicit or documented; it operates through market signals, shared intelligence, and implicit coordination.

How much does broker collusion cost commodity traders?

Broker collusion typically costs commodity traders 15–25% of their annual freight spend in excess rate premiums. For a mid-market trading desk with $6 million in annual freight expenditure, this translates to $900,000–$1.5 million per year. Over five years, the cumulative cost can reach $4.5–$7.5 million. These costs are difficult to detect because they appear as "market rates" — the trader has no visibility into what a genuinely competitive process would have produced.

How does closed-bid tendering prevent broker collusion?

Closed-bid tendering prevents collusion by isolating each broker's bid. Brokers receive individual invitations through a controlled platform, submit structured offers without any visibility into what other brokers are bidding, and cannot revise their submissions after the fact. This eliminates the information-sharing that enables rate coordination. Across Bench Energy's client base managing $1.2B+ in freight, closed-bid tendering has delivered an average 18% rate reduction compared to email tendering.

Related articles

- Closed-Bid Freight Tendering: Why Sealed Offers Beat Email Tenders

- Why Email Tendering Fails Commodity Traders

- How to Negotiate Freight Rates in a Volatile Market

- The Complete Freight Procurement Guide for Commodity Traders

Related: Email tendering problems · Dubai commodity traders · Geneva trading market · Singapore trading hub · FreightTender platform · Calculate your savings

Quantify the cost of broker collusion

Multiply your annual freight spend by 15% — that's the conservative estimate. Request a demo or use the ROI calculator.

Build your trading vocabulary

Commodity & Freight Trader's Lexicon

200+ Anki flashcards covering coal, metals, and oil trading — charter party clauses, laytime mechanics, FOB/CIF structures, price indices, and market terminology used by professional traders.