Broker Collusion in Freight Tendering: $1M+/Year Cost & Closed-Bid Fix

Key Takeaways

- Forwarded threads reveal who else was invited

- Brokers read urgency from laycan and cargo specs

- Offers arrive in a narrow band — sometimes within 2–3% on routes where independent views should be wider

- Late revisions appear after one broker learns another's level

Physical traders negotiate hard on cargo — then run freight on email to the same 15 brokers in Dubai, Geneva, or Singapore. The issue is rarely a single bad quote. It is a thin spread when everyone has the same market colour.

How signalling shows up

Freight brokerage is a small, relationship-driven market. On an email RFQ to five brokers:

- Forwarded threads reveal who else was invited

- Brokers read urgency from laycan and cargo specs

- Offers arrive in a narrow band — sometimes within 2–3% on routes where independent views should be wider

- Late revisions appear after one broker learns another's level

That is informal bid signalling — not necessarily illegal collusion, but weak competition for the desk.

What it costs (measure yours)

Do not use a generic industry %. On your last 20 tenders, record:

- Spread between highest and lowest broker quote (same cargo spec)

- Awarded rate vs Baltic or route benchmark you trust

- Hours from RFQ send to award

If spreads are consistently tight and awards sit above index, the process — not the market — is the first place to fix.

Why email enables it

Email has no bid isolation, no single comparison table, and no standard award file. Finance and audit see outcomes in CTRM, not the negotiation path.

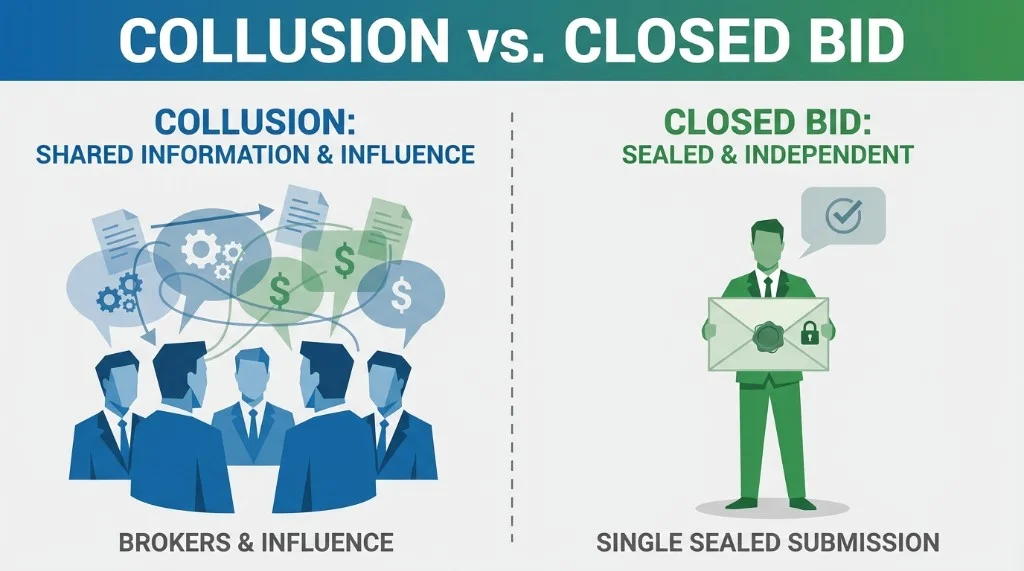

What helps

- Sealed bids — each broker sees only their invitation (closed-bid tendering)

- Larger, rotated panels — do not invite the same five brokers every time (broker panel design)

- Bid spread test — run the same cargo twice with different panel rules (bid spread test)

- Benchmark at award — index or route reference beside each quote (RFQ benchmarking)

Red flags to track

- Offers cluster within a few percent on competitive routes

- Same brokers win in a fixed rotation without vessel/market reason

- Awards persistently above your benchmark strip

- Multiple bids land within minutes with near-identical laytime clauses

One odd tender is noise. A quarter of repeats is systemic.

Worked example (illustrative)

A coal desk runs 120 spot fixtures/year at roughly $50k average freight (~$6M annual spend). After moving RFQs to sealed bids and a rotated 12-broker panel, they tracked:

- Wider best-vs-worst spread on identical specs

- Faster awards (same-day on most cargoes)

- Exportable award files for internal review

Your numbers will differ by commodity, corridor, and panel — run a five-tender pilot against your email baseline.

FAQ

What is informal bid signalling?

Convergence of broker quotes when market colour is shared on email RFQs — through relationships, timing signals, or visibility into the panel — rather than independent pricing.

How much does it cost?

Depends on your volume and spread. Benchmark 20 fixtures; multiply any persistent premium by annual tonnage and fixtures.

How do sealed bids help?

They remove cross-bid visibility and produce one normalized table plus a timestamped award rationale.

Related

Related: Email tendering problems · FreightTender · ROI calculator

Get a 10-minute RFQ leakage audit

Find leakage in your brokered freight RFQs

Bring one recent RFQ. We map offer comparison, benchmark gap, timing risk, and award record — no commitment.

Quantify the cost of broker collusion

Multiply your annual freight spend by 15% — that's the conservative estimate. Get an RFQ leakage audit or use the ROI calculator.

Build your trading vocabulary

Commodity & Freight Trader's Lexicon

200+ Anki flashcards per deck — charter party clauses, laytime, FOB/CIF, indices, and desk terminology. Instant download after checkout on Gumroad.